Introduction

Building wealth isn’t about finding a magic investment or getting lucky once. It’s the practical habit of turning your pay into a plan, then letting time and smart choices do the heavy lifting. If you’re searching for “how to build wealth step by step are you missing this,” you’re probably already saving some money, but you might not have a clear system that keeps you moving when life gets busy.

The common missing step is usually not math or motivation. It’s getting your money organized around a goal, so you know what to do next, what to avoid, and how to measure progress. When you do that, wealth building becomes less confusing and more repeatable. You’re not guessing anymore, you’re following steps.

Key Takeaways

- Wealth building works best with a measurable goal (numbers + timeline) tied to your real life priorities, so you know what to do and what to avoid.

- Create a monthly cash-flow map: income, fixed bills, variable spending, then set a “leftover money” target for saving, debt payoff, and investing.

- Pay off high-interest debt first using a strategy you can stick with (avalanche for lowest interest cost, snowball for motivation).

- Build an emergency fund to prevent surprises from forcing new credit-card debt; start small if needed and keep it accessible.

1. Define your “how to build wealth” goal with numbers

Start with a goal you can actually measure, because “get rich” is too vague to guide decisions. Pick a timeframe, like three to five years for a first milestone or ten years for bigger moves. Then choose a measurable target, such as saving a specific amount, investing a set monthly dollar figure, or reaching a net worth number.

Next, connect the goal to real lifestyle priorities and constraints. If you want to buy a home, your target may include a down payment timeline and the cash you need to keep safe. If you want financial freedom, you’ll think differently about debt payoff, emergency reserves, and how much you can invest consistently. Keep the goal realistic enough that you’ll stick with it, even when unexpected expenses pop up.

Wealth building gets easier when your goal acts like a GPS, not a wish. Numbers help you choose, say no, and stay consistent.

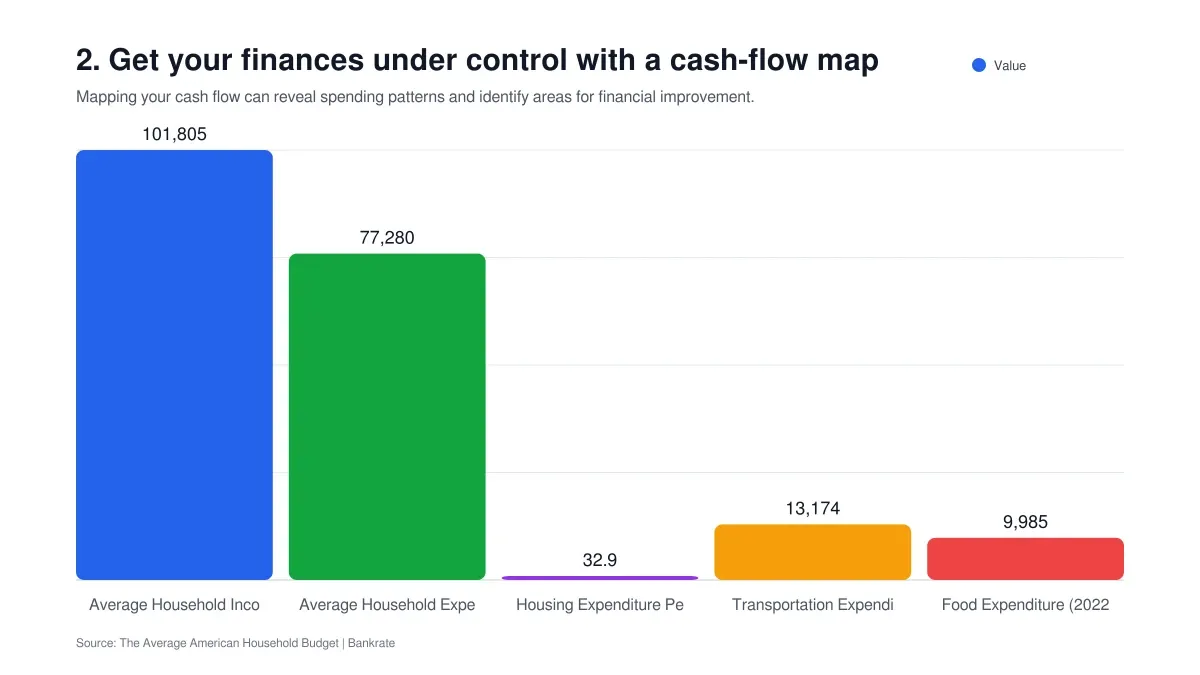

2. Get your finances under control with a cash-flow map

Before you chase bigger returns, map your cash flow so you know where your money is going each month. Track your income first, then list fixed bills like rent, utilities, insurance, and minimum debt payments. After that, add variable spending categories such as groceries, eating out, transport, and subscriptions. This makes patterns visible, and patterns are where you find easy wins.

Then build a “leftover money” target. That’s the portion of your income that remains after bills, which you can split into saving, debt payoff, and investing. A simple way to set it is to pick a percentage or dollar amount you want to move every month, then adjust the budget categories until it becomes possible. If your leftover money is negative, that’s not failure, it’s information. It means you need a spending cut, a bill reduction, or more income before investing can grow.

- Income, fixed bills, variable spending, then leftover money

- Keep it monthly so you can compare like with like

- Review it weekly for the first month, then monthly

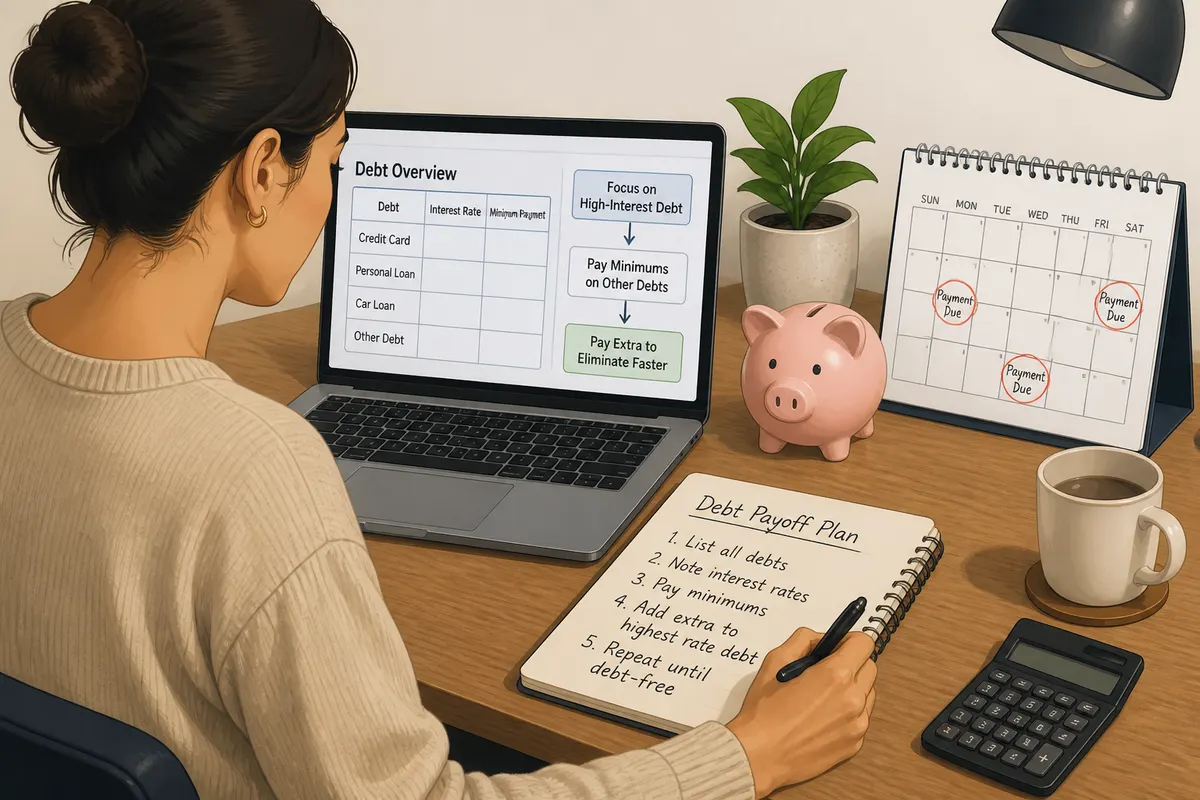

3. Eliminate high-interest debt before pushing harder

High-interest debt can silently drain your wealth, because it often costs more than what you might earn through investing. Take time to list all debts, including credit cards, personal loans, car loans, and any other balances. For each one, write down the interest rate and the minimum payment so you can see which debts are costing you the most each month.

Once you know where the damage is, choose a payoff strategy that you can stick with. The “avalanche” approach targets the highest interest rate first, which is usually the most efficient over time. The “snowball” approach targets the smallest balance first, which can be motivating because you get quick wins. Neither is magic, but your best choice is the one that keeps you paying consistently until the debt is gone.

| Strategy | What You Pay First | Main Benefit | Best If You |

|---|---|---|---|

| Avalanche | Highest interest rate | Often saves more money on interest | Prefer math-based decisions and steady discipline |

| Snowball | Smallest balance | Creates momentum with faster payoff | Need motivation to keep going |

Important: If you’re behind on payments or dealing with collections, consider contacting lenders for hardship options. Reducing stress helps you stay on track.

4. Build an emergency fund that protects your plan

An emergency fund is money set aside for surprises, like medical bills, car repairs, or job gaps. Without it, emergencies often force you to use credit cards, which restarts the debt cycle you worked hard to end. So the goal is protection first, not investment thrills.

The right emergency-fund size depends on your situation. If your income is stable and expenses are predictable, you may aim for a smaller starter fund first, then build toward a larger buffer. If you have variable income, dependents, or higher risk in your job, you’ll likely want more. Many people start with a short-term goal like having a few hundred to a couple thousand dollars, then expand from there.

Keep the fund accessible without making it too tempting to spend. That usually means a separate, easy-to-reach account, not your everyday checking balance and not long-term investments. A good rule is simple: you can use it for true emergencies, not for planned purchases or “just this once” upgrades.

- Start small, then scale up

- Separate it from spending money

- Only use it for real emergencies

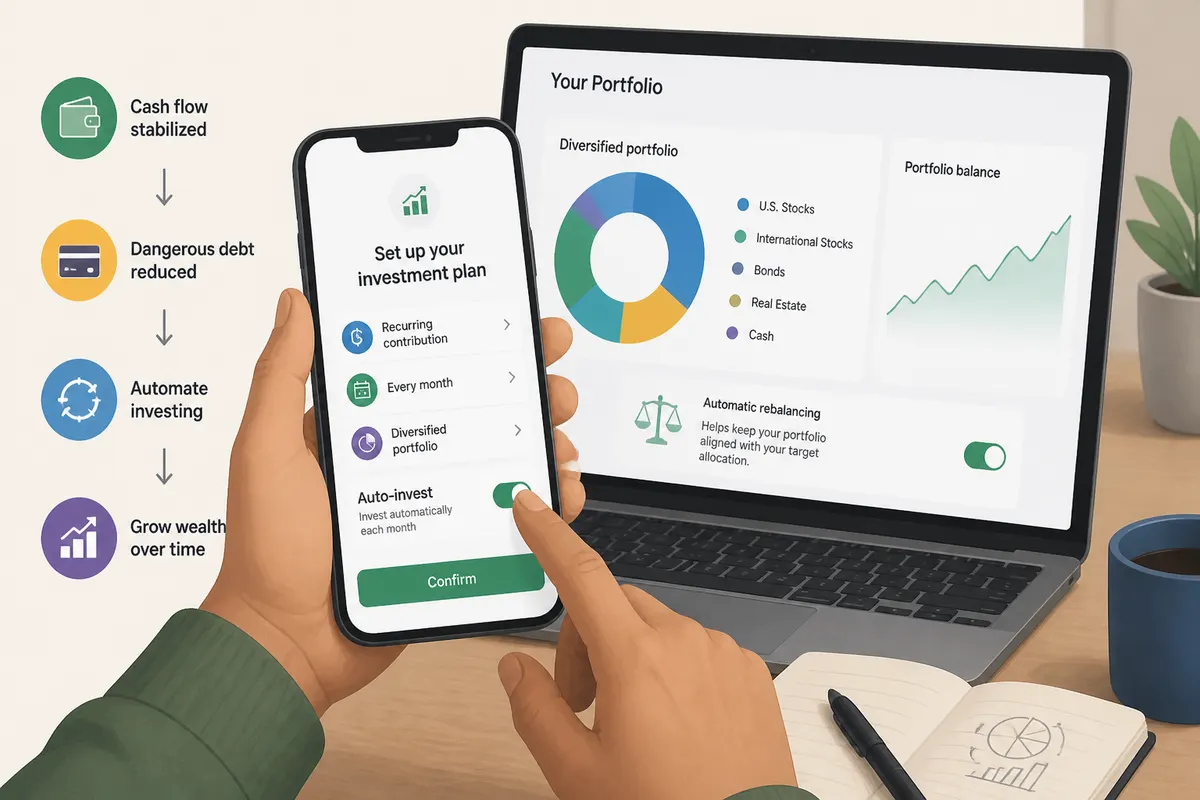

5. Start investing automatically with simple, diversified choices

Once you’ve stabilized your cash flow and reduced dangerous debt, investing can help your money grow over time. The easiest way to stay consistent is automation. Set up recurring contributions, so you invest regularly instead of trying to time the market. Also consider simple automatic rebalancing, or at least check your mix periodically so your risk doesn’t drift.

Diversification matters because it reduces the risk of relying on one company or one asset type. Instead of buying a handful of individual stocks, many investors use diversified funds to spread exposure across many holdings. This can lower the impact of any single poor performer. Think of it like not putting all your groceries in one bag.

Still, keep expectations realistic. Investing involves ups and downs, and short-term performance can look ugly. Your job is to choose sensible building blocks, invest consistently, and avoid big changes based on headlines.

- Use recurring contributions, so investing happens on schedule

- Choose diversified options to reduce single-asset risk

- Recheck your allocation when life changes

6. Increase income in ways that fit your skill set

Saving and investing matter, but increasing income often speeds up everything. Look for ways that fit your experience and strengths, like negotiating pay, switching roles, or taking on responsibilities that lead to higher pay. Even small raises can add up when you consistently invest the difference.

For many people, side income is helpful, as long as it doesn’t derail your money plan. Choose something you can manage without burning out, and that fits your schedule. Then treat the extra income like a dedicated “wealth contribution,” meaning you automate part of it into savings or investing right away. That way, you don’t fall into the trap of spending every new dollar.

One practical approach is to compare options by time and effort, not just potential earnings. A job change with better pay might beat a side hustle that’s profitable but draining. The best path is the one you can sustain long enough for compounding to work.

A raise that you invest automatically is often more powerful than a big one-time bonus you might spend.

7. Track progress and rebalance your wealth plan regularly

If you want wealth building to keep moving, track progress instead of guessing. Measure net worth over time, which is basically what you own minus what you owe. Also track investment contributions, since consistent deposits matter even when markets are bumpy. A simple monthly check-in keeps you aware of where things stand.

Then rebalance your plan when needed, especially if your risk level changes due to market moves or life updates. If your expenses rise, you might need to adjust how much you invest. If your goal changes, like a new home timeline or a new family responsibility, you’ll want your emergency fund and investment plan to match. Your “risk tolerance” is how much fluctuation you can handle without panicking and making bad decisions.

Life changes, so your plan should flex. But avoid the temptation to make frequent big shifts based on emotion. Use your system, review the numbers, and make changes with a reason you can explain.

- Check net worth and contributions monthly or quarterly

- Update budgets when income or costs change

- Rebalance if your target mix drifts too far

Conclusion

Here’s the step-by-step checklist to start building wealth this month. Set a measurable goal with a timeframe, then map your cash flow to find your leftover money. Eliminate high-interest debt using avalanche or snowball, and protect your progress with an emergency fund you can access. After that, start investing automatically with simple, diversified choices, while increasing income in ways that match your skills.

Finally, track net worth and contributions, then rebalance when life changes. Your next action is pick one step you can do in the next seven days, and set a realistic deadline. If you’re looking for how to build wealth and the missing piece is consistency, this plan is designed to give you exactly that, one clear move at a time.

Frequently Asked Questions

How to build wealth step by step – what’s the first missing step people overlook?

The most common missing step is not motivation or “secret math.” It’s organizing your money around a specific, measurable goal so you always know what to do next, what to avoid, and how to track progress – especially when life gets busy.

How do I define a measurable “how to build wealth” goal with numbers?

Start by choosing a timeframe (e.g., a few years for an early milestone or longer for a bigger goal). Then set a target you can measure, such as a specific savings amount, a monthly investment dollar figure, or a net worth milestone. The key is turning vague goals into trackable numbers.

What timeframe should I use when learning how to build wealth?

Use a timeframe that matches your first milestone and your realistic ability to adjust. Many people set a shorter horizon (like 3-5 years) for an initial target and a longer horizon (like 10 years or more) for larger outcomes such as financial freedom or major asset goals.

How do lifestyle priorities and constraints change my wealth-building plan?

Your plan should connect to real-life needs like buying a home, managing debt, maintaining emergency cash, and investing consistently. For example, a home goal usually requires a down payment timeline and safe cash reserves, while a financial freedom goal changes how you prioritize debt payoff and long-term investing.

If I’m already saving money, why do I still need a wealth-building system?

Saving helps, but without a system tied to a goal you may not know what to do next or how to measure progress. A goal-based system reduces guesswork by clarifying actions, trade-offs, and metrics – so your plan stays consistent even during disruptions.

What should I measure to know I’m progressing with how to build wealth?

Track measurable indicators connected to your goal, such as how much you’ve saved or invested versus your target, whether your debt is trending down if that’s part of the plan, your net worth progress, and whether you’re maintaining required buffers like emergency savings.

How do I avoid guessing when building wealth over time?

Replace guessing with repeatable steps: set a measurable goal and timeframe, translate it into actionable categories (spending limits, savings/investing amounts, and debt priorities), and use progress metrics to guide decisions. This turns wealth building into a process you can follow – not a one-time lucky outcome.

What’s the difference between building wealth for a home vs building wealth for financial freedom?

A home-focused plan often centers on accumulating a down payment within a specific timeline and keeping enough cash safe for near-term needs. A financial-freedom plan typically emphasizes reducing high-interest debt, maintaining adequate emergency reserves, and investing a consistent monthly amount to reach long-term goals.

Sources

Build Wealth Over Time Through Saving and Investing | Investor.gov

{kind=link}