Introduction

If you keep skipping money basics, your “wealth plan” usually turns into guesswork. And guesswork is expensive, because fees add up, interest piles on, and inflation quietly shrinks what you thought was growing. That is where wealth education becomes useful because it turns the opening concern into a repeatable plan.

That’s why wealth education matters, but it needs to be in plain language. In this beginner’s glossary, we’ll define the terms you’ll see in budgeting, saving, investing, and planning, then show you how to use the list like a learning tool. Read one section, pick one term, and apply it to your own money situation before you move on. If you do that, you’ll build confidence fast, without needing a finance degree.

Key Takeaways

- A budget is your monthly plan, cash flow tracks money in/out over time, and net worth shows assets minus debts as your financial snapshot.

- Inflation and purchasing power matter: higher prices can erase “progress,” so focus on what your money can actually buy over time.

- An emergency fund size depends on your life; prioritize liquidity and safety, keep it separate for essentials, and review as income/expenses change.

- Debt costs aren’t mystery: APR and compounding drive total interest, and paying only minimums can prolong debt and increase cost.

- Investing basics: stocks vs bonds, diversify with ETFs/mutual funds, and watch fees/expense ratios since small costs can compound over years.

Wealth Education Terms Everyone Should Know First

Start with a simple map. A budget is your plan for where your money goes each month. Cash flow is the money coming in and going out over time, like a monthly stream. Net worth is the snapshot, assets minus debts, so you can see where you stand even when you feel stuck.

Next, learn how to think about outcomes. Risk means the chance your investment or plan could go down. Return is what you earn, usually in dollars, and time horizon is how long you can stay invested before you need the money. Then there’s inflation, which is rising prices over time, and purchasing power, which is what your money can actually buy. More money isn’t always better, because higher prices can cancel out the feeling of progress.

Savings and Emergency Funds: The Non-Negotiables

A savings account is your “stability tool,” and the interest rate matters because it changes how fast your balance grows. High-yield savings accounts often offer a higher rate than basic checking or standard savings, but they still tend to stay relatively low risk compared to investments. Use interest as a small reward while your bigger goals, like investing or paying down debt, stay in the background.

For emergency funds, the best size depends on your life, not someone else’s rulebook. Many people aim for several months of essential expenses, like housing, food, and transportation, because emergencies rarely happen on a calm timeline. Two trade-offs matter: liquidity means you can access cash quickly, and safety means your balance is less likely to drop. The downside is that cash earns less than stocks over long periods, so you want enough safety, then move excess money toward higher-growth plans.

- Essentials only for your emergency estimate, not “nice to have” spending.

- Keep it separate from daily spending so you’re less tempted to use it casually.

- Review yearly when your income or expenses change.

Debt Literacy: Paying Less Interest, Faster

Debt can feel like a black box, so let’s open it. APR (annual percentage rate) is the yearly interest rate you’re charged, and it helps you compare loans. Interest can also compound, meaning interest builds on top of interest, which is why small balances can grow faster than you expect. Then there are minimum payments, which are designed to keep the account current, but they can stretch payoff time and cost you more overall.

Debt also comes in different forms. Secured debt is backed by something you can lose, like a car or a home, while unsecured debt isn’t tied to a specific asset. The repayment risk is higher with secured debt, because losing collateral can be life-changing. When you pay it down, two common methods are the avalanche, which targets the highest interest first, and the snowball, which targets the smallest balance first to build momentum. Pick the one you’ll stick with, because consistency beats perfect math.

| Payoff Method | What It Targets | Why It Works | Best For |

|---|---|---|---|

| Avalanche | Highest APR first | Usually reduces total interest paid | You want the most cost savings |

| Snowball | Smallest balance first | Creates quick wins and motivation | You need momentum to stay on track |

Payoff progress is math and behavior, so choose the plan that matches both your numbers and your real habits.

Investing Basics: Portfolios Without the Jargon

Investing starts with understanding what you’re buying. Stocks are ownership in a company, and they can rise or fall with business results and market mood. Bonds are loans to governments or companies, and they often aim to provide steadier income than stocks. ETFs and mutual funds are baskets of investments, which makes diversification easier for beginners, because you buy many holdings at once.

Diversification matters because concentration can hurt. Diversification means spreading money across different assets so one bad outcome doesn’t wreck everything. Correlation is how closely two investments move together, and it’s a big reason people avoid an “all-in” single bet. Also, watch fees and expense ratios, which are the ongoing costs for running funds. Even small costs can compound quietly over years, so it’s worth comparing what different funds charge.

- Match investments to your goals and time horizon, not your emotions.

- Use fund baskets like ETFs or index funds to build diversification fast.

- Keep an eye on total costs, including fund expenses and trading costs.

Retirement and Accounts: Where Your Money Can Grow

Retirement investing often uses tax-advantaged accounts, which are accounts designed to change how taxes work on your money. That could mean you pay less tax now, or later, depending on the account type. While the exact rules vary by country, the idea is the same: tax treatment can improve your after-tax returns, even when the investment choices are similar.

Two practical things you should understand are contribution limits and employer help. Many plans have annual caps for how much you can contribute, and some employers offer a match, which is extra money if you contribute enough. Also pay attention to account rules, like eligibility, deadlines, and where contributions can come from.

Finally, learn the basics of withdrawals. Vesting applies when an employer contributes funds, and it determines when you truly own those contributions. Withdrawals can be restricted, and penalties often apply if you take money out too early. Reading the “how it works” section of your account helps you avoid surprises.

Wealth Protection and Planning: Staying Ahead of Surprises

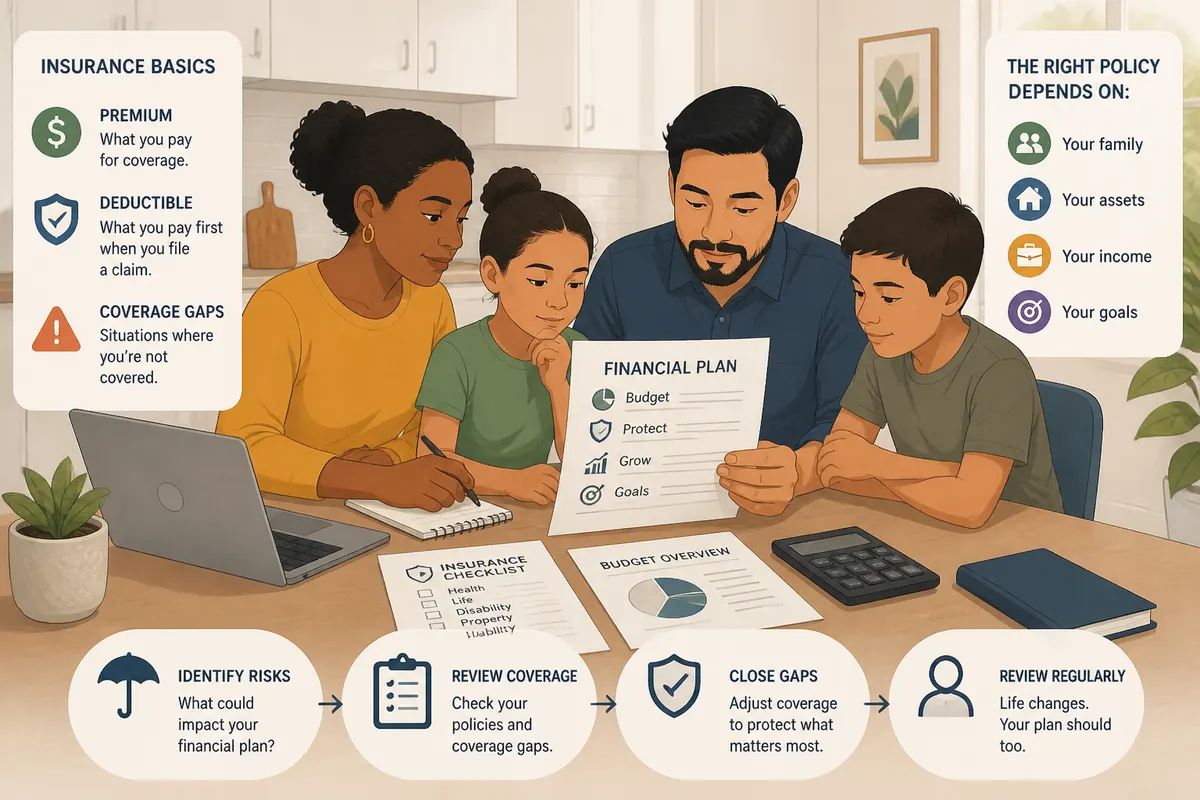

Wealth protection isn’t about fear, it’s about planning for the stuff you can’t control. Insurance basics are a good starting point: a premium is what you pay for coverage, a deductible is what you pay first when you file a claim, and coverage gaps are the situations where you’re not covered. The right policy depends on your risks, like your health, your home, your car, and your income.

Next, handle the planning side of “what happens if.” Estate planning uses tools like wills, which describe how you want assets distributed, and trusts, which can provide extra control in some cases. You’ll also see beneficiaries, the people or accounts listed to receive certain assets. These choices matter because they can reduce confusion for the people who act on your behalf.

And don’t forget emergency planning for finances. Keep key documents easy to find, like account statements, insurance policies, and a list of where money sits. If you use passwords, consider a secure way to grant access to a trusted person. Simple organization today can save big headaches later.

- Recheck insurance coverage after big life changes.

- Update beneficiaries when major events happen, like marriage or new dependents.

- Store documents in one safe, accessible location.

Conclusion

Wealth education becomes much easier when you translate finance jargon into everyday meaning. Once you understand budget, cash flow, net worth, risk, and inflation, you can make smarter choices without feeling lost. Then you build stability with an emergency fund, reduce costly debt, and start investing with a clear idea of what you own and why diversification matters.

Keep moving one step at a time, and let your learning connect to your real money decisions. If you use this beginner’s glossary as a checklist while you plan, your progress will feel more grounded and less stressful, which is exactly what wealth education is supposed to do.

{kind=link}